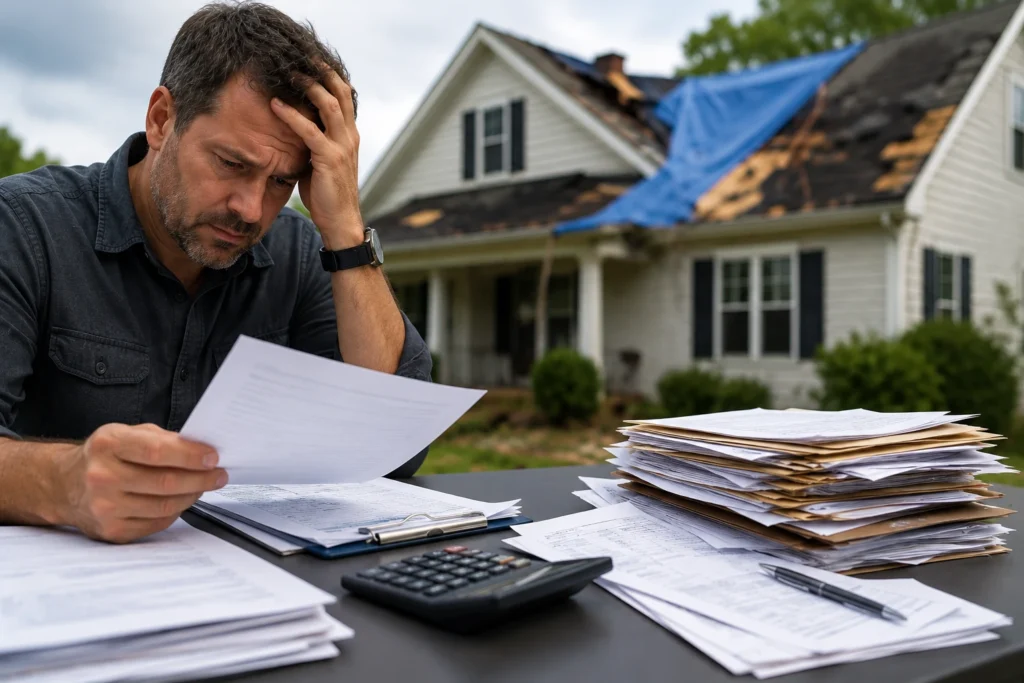

Insurance claims can be frustrating, especially when the payment you receive is lower than expected. In many cases, the difference comes from withheld depreciation. Understanding Recoverable Depreciation Explained helps homeowners recover funds that may still be available under their insurance policy. Moreover, knowing how the process works can prevent costly mistakes and improve claim outcomes.

What Is Recoverable Depreciation?

At its simplest, recoverable depreciation is the amount of depreciation an insurance company temporarily withholds from a claim settlement until repairs or replacements are completed. Insurance companies recognize that building materials and property components lose value over time. For example, a 15-year-old roof is not worth the same as a brand-new roof. Because of this, insurers often calculate two values:

- Actual Cash Value (ACV)

- Replacement Cost Value (RCV)

The difference between these two amounts is frequently the recoverable depreciation. Once repairs are completed and proof is provided, the insurer may release the withheld depreciation payment.

How Recoverable Depreciation Works

Typically, the process follows these steps:

- Property damage occurs.

- Insurance company inspects the loss.

- Claim estimate is prepared.

- Depreciation is deducted.

- Initial ACV payment is issued.

- Repairs are completed.

- Documentation is submitted.

- Recoverable depreciation is released.

Many policyholders mistakenly believe the first check represents the entire settlement. However, it often does not.

Example of Recoverable Depreciation

| Claim Component | Amount |

|---|---|

| Replacement Cost Value | $20,000 |

| Depreciation Withheld | $5,000 |

| Initial ACV Payment | $15,000 |

| Recoverable Depreciation | $5,000 |

In this example, the homeowner receives $15,000 initially. Afterward, once repairs are completed and documentation is submitted, the remaining $5,000 may be paid. This is one of the most important concepts when discussing Recoverable Depreciation Explained because many homeowners never realize additional money is available.

Understanding Actual Cash Value vs. Replacement Cost Value

Before discussing depreciation further, it helps to understand the two valuation methods used in property insurance.

What Is Actual Cash Value?

Actual Cash Value represents the property’s replacement cost minus depreciation. Insurance companies consider factors such as:

- Age

- Wear and tear

- Condition

- Expected lifespan

As property components age, their value decreases. For example, a roof that originally cost $20,000 may have an ACV of only $12,000 after years of use.

What Is Replacement Cost Value?

Replacement Cost Value represents the amount needed to replace damaged property with materials of similar quality at current market prices. As a result, RCV generally provides better financial protection because it reflects today’s replacement costs rather than depreciated values. Most homeowners prefer replacement cost coverage because construction expenses continue to rise.

ACV vs. RCV Comparison

| Actual Cash Value | Replacement Cost Value |

|---|---|

| Depreciation deducted | Full replacement cost available |

| Lower settlement | Higher settlement |

| Lower premiums | Higher premiums |

| No depreciation recovery | Recoverable depreciation available |

Understanding this distinction is essential when discussing Recoverable Depreciation Explained because policy language often determines whether withheld depreciation can be recovered.

Why Insurance Companies Withhold Recoverable Depreciation

Many homeowners assume the insurance company is simply trying to reduce claim payments. In reality, the situation is more nuanced.

Preventing Overpayment

Insurance companies generally release recoverable depreciation only after repairs are completed. Consequently, this requirement helps ensure claim funds are used for their intended purpose. Without this safeguard, insurers could potentially pay full replacement costs for repairs that never occur.

Verification of Actual Costs

Construction costs frequently vary from estimates. Some repairs cost less. Others cost more. Therefore, by waiting until repairs are complete, insurers can verify the actual amount spent on restoration.

Policy Compliance

Most replacement cost policies contain conditions that must be satisfied before depreciation is released. These conditions often include:

- Completing repairs

- Meeting policy deadlines

- Providing invoices

- Submitting proof of payment

Otherwise, failure to meet these requirements can delay or jeopardize recovery of depreciation.

What Types of Claims Include Recoverable Depreciation?

Recoverable depreciation appears in many types of property claims.

Roof Damage Claims

Roof claims commonly involve significant depreciation amounts. This is especially true when older roofing systems are damaged by:

- Hail

- Wind

- Falling trees

- Severe storms

Texas homeowners frequently encounter recoverable depreciation in roof replacement claims because roofing materials naturally depreciate over time.

Water Damage Claims

Water losses may include depreciation related to:

- Flooring

- Cabinets

- Drywall

- Baseboards

- Paint

Furthermore, the withheld amount can become substantial when multiple rooms require restoration.

Fire Damage Claims

Fire claims often involve:

- Structural repairs

- Smoke remediation

- Electrical systems

- Interior finishes

Likewise, large fire losses can generate significant depreciation holdbacks that policyholders must actively pursue.

Hurricane and Severe Weather Claims

Major weather events often create extensive property damage. As claim values increase, depreciation amounts typically increase as well. Therefore, understanding Recoverable Depreciation Explained becomes even more important after major storms.

How Recoverable Depreciation Is Calculated

No two claims are identical. Instead, insurance companies evaluate several factors when calculating depreciation.

Age of Materials

Older components generally receive higher depreciation deductions. Examples include:

- Roofing systems

- HVAC equipment

- Flooring materials

- Exterior siding

The closer a component is to the end of its expected lifespan, the greater the depreciation.

Condition Before the Loss

Maintenance matters. A well-maintained roof may receive less depreciation than a neglected roof of the same age. Insurance adjusters often evaluate:

- Prior repairs

- Maintenance records

- Visible wear

- Overall condition

Expected Useful Life

Each building component has a projected service life. Insurance companies rely on statistical models when estimating risk, depreciation, and claim costs. Many of these calculations are influenced by principles found in actuarial science, which helps insurers evaluate financial risk over time.

| Component | Typical Useful Life |

|---|---|

| Asphalt Roof | 20–30 Years |

| Carpet | 5–15 Years |

| HVAC System | 15–20 Years |

| Exterior Paint | 5–10 Years |

| Wood Flooring | 20–50 Years |

The useful life assigned to roofing, flooring, and other building materials often reflects long-term durability studies. Similar evaluation methods are used in life-cycle assessment, which examines the lifespan and performance of products throughout their existence. As a result, depreciation calculations frequently depend on how much of that useful life has already been consumed.

Reviewing the Insurance Estimate

One of the smartest things a homeowner can do is carefully review the insurance estimate. Do not skip this step. Look specifically for:

- Depreciation line items

- ACV amounts

- RCV amounts

- Holdback calculations

- Notes regarding payment conditions

Many policyholders discover discrepancies simply by reading the estimate carefully. The claim paperwork often reveals exactly how much depreciation is being withheld and what steps are required to recover it.

The Steps to Recover Depreciation After a Claim

Knowing recoverable depreciation exists is only half the battle. More importantly, homeowners must understand how to actually obtain those withheld funds.

Complete the Repairs

In most situations, insurers require repairs to be completed before releasing recoverable depreciation. This typically involves:

- Hiring qualified contractors

- Replacing damaged materials

- Completing approved restoration work

- Meeting policy requirements

However, every policy is different, so reviewing your coverage remains essential.

Save All Documentation

Documentation can make or break a claim. Therefore, keep copies of:

- Contractor contracts

- Paid invoices

- Material receipts

- Before-and-after photographs

- Inspection reports

The more organized your records are, the easier the process becomes.

Submit Proof of Completion

Once repairs are finished, notify your insurance company immediately. Most insurers request documentation showing that repairs have been completed according to the approved scope of work.

Request Release of Depreciation

Do not assume payment will automatically arrive. Instead, follow up with your adjuster and formally request release of the recoverable depreciation amount. Prompt communication often prevents unnecessary delays.

Common Reasons Recoverable Depreciation Is Delayed

Even valid claims can experience delays. Fortunately, many of the most common issues can be avoided.

Missing Documentation

Incomplete paperwork remains one of the leading causes of delayed depreciation payments. Missing receipts, unpaid invoices, or incomplete contractor documentation often slow the review process.

Incomplete Repairs

If repairs are only partially completed, insurers may decline to release the full depreciation amount. As a result, homeowners should ensure all required work has been finished before requesting payment.

Disputes Over Scope of Work

Sometimes contractors identify additional damage that was not included in the original estimate. This can create disagreements regarding repair costs and payment amounts.

Policy Deadlines

Most policies contain deadlines for completing repairs and requesting depreciation reimbursement. Missing these deadlines can create serious complications. Therefore, it is important to review policy requirements early in the claims process.

Can You Recover Depreciation If You Perform Repairs Yourself?

Many homeowners choose to complete certain repairs on their own. While this can reduce costs, it may affect depreciation recovery.

Understanding Self-Performed Repairs

Insurance policies vary considerably. Some insurers reimburse material costs but limit compensation for personal labor. Others may require extensive documentation before approving reimbursement.

Documentation Still Matters

Even when performing repairs yourself, maintain detailed records. Helpful documentation includes:

- Material receipts

- Project photographs

- Supply invoices

- Completion records

The stronger the documentation, the stronger the reimbursement request.

Deadlines for Recovering Depreciation

Time matters. Many homeowners lose recoverable depreciation simply because they wait too long.

Policy Time Limits

Depending on the policy, deadlines may range from six months to several years after the loss. However, every insurance contract is different. Always verify the specific deadline contained in your policy.

Request Extensions When Necessary

Large projects occasionally take longer than expected. Contractor shortages, permit delays, and severe weather can slow repairs. In those situations, requesting an extension before the deadline expires may help preserve your rights.

Common Mistakes Homeowners Make

Recoverable depreciation is often lost due to avoidable mistakes.

Failing to Read the Insurance Estimate

Many policyholders never review the estimate carefully. Consequently, they may not realize depreciation is being withheld.

Throwing Away Receipts

Receipts provide evidence of repair costs. Without them, recovering depreciation can become significantly more difficult.

Waiting Too Long

Delays create problems. Therefore, begin repairs and maintain communication with your insurer whenever possible.

Assuming Depreciation Is Automatic

One of the most common misconceptions is that insurers automatically release withheld depreciation. In reality, policyholders often must request payment and provide supporting documentation.

What Happens When Recoverable Depreciation Is Underpaid?

Not every depreciation dispute involves a denial. Sometimes the issue involves an underpayment.

Reviewing the Insurance Scope

Start by comparing the insurer’s estimate with contractor proposals and completed repair costs. Look for:

- Missing items

- Underpriced materials

- Incomplete repair recommendations

- Labor discrepancies

Can You Dispute a Scope of Loss?

Many homeowners eventually ask, “Can You Dispute a Scope of Loss?” The answer is yes. If the insurance company’s estimate omits necessary repairs, undervalues materials, or overlooks damaged areas, policyholders can challenge the scope through supplemental documentation, contractor estimates, engineering reports, or the appraisal process. Reviewing the scope carefully is often a critical step when attempting to recover withheld depreciation and secure a fair claim settlement.

Obtaining Independent Estimates

Independent contractor estimates frequently identify overlooked damage. Additionally, they may provide valuable evidence when challenging underpaid claims.

Requesting Claim Reconsideration

If discrepancies exist, policyholders can request a claim review. Providing additional documentation often strengthens the request.

When the Appraisal Clause May Help

Some insurance policies include an appraisal clause. This provision allows disputes regarding claim value to be resolved without litigation. Although appraisal does not determine coverage, it can help resolve disagreements over the amount of loss.

How Insurance Appraisers Help With Recoverable Depreciation Disputes

Insurance appraisers frequently become involved when claim values are disputed.

Reviewing Estimates

Appraisers analyze insurer estimates and compare them to actual repair requirements. This review often uncovers omitted items or valuation issues.

Identifying Missing Damage

Hidden damage sometimes goes unnoticed during initial inspections. As a result, supplemental claim opportunities may emerge.

Supporting Appraisal Proceedings

When disputes escalate, appraisers can provide professional evaluations regarding the amount of loss. Their findings often play a significant role in claim resolution.

Improving Claim Accuracy

Ultimately, accurate valuations benefit everyone involved. Proper claim evaluation helps ensure recoverable depreciation is calculated fairly.

Texas-Specific Considerations for Recoverable Depreciation Claims

Texas homeowners face unique property risks.

Severe Weather Losses

Texas regularly experiences:

- Hailstorms

- Windstorms

- Hurricanes

- Tornadoes

These events frequently generate claims involving substantial depreciation amounts.

Documentation Is Critical

Because storm-related claims can involve extensive repairs, maintaining thorough documentation becomes even more important. Photos, receipts, contractor estimates, and inspection reports often prove invaluable.

Understanding Your Rights

Texas policyholders have options when disputes arise. Whether through supplemental claims, negotiation, or appraisal, understanding available remedies can help homeowners pursue fair claim outcomes.

Conclusion

Understanding Recoverable Depreciation Explained helps homeowners avoid leaving money on the table after a property loss. While insurers often withhold depreciation initially, those funds may become recoverable once repairs are completed and properly documented. Therefore, reviewing your estimate, keeping detailed records, and understanding your policy requirements can make a significant difference. If disputes arise, professional guidance and appraisal options may help ensure you receive the full value of your claim.

FAQs

Recoverable depreciation is the portion of an insurance claim payment that is withheld until repairs or replacements are completed and documented.

Review your policy declarations or speak with your insurer to determine whether you have replacement cost coverage that includes recoverable depreciation.

The timeline varies, but insurers typically release the payment after receiving proof that repairs have been completed.

In most cases, yes. Receipts, invoices, and contractor documentation help verify repair costs and support your request.

Possibly. Some policies allow recovery of material costs, but reimbursement for personal labor may be limited.

You may be able to submit supplemental documentation and request additional claim consideration from the insurer.

Yes. Missing documentation, incomplete repairs, or failure to meet policy requirements can result in denial of the withheld amount.

Yes. Roof replacement claims frequently include recoverable depreciation because roofing materials lose value as they age.

Yes. If the depreciation calculation appears inaccurate, you can provide supporting evidence and request a review.

An insurance appraiser may help evaluate the claim, identify valuation issues, and support dispute resolution when disagreements arise.